老师课堂留下的思考题是:

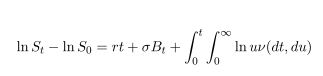

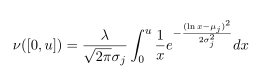

8. Assuming the stock price is driven by a mixed Poisson-Brownian motion with stock return

to be given by

with Levy measure to be given by

Let r = 8%,σ = 12%,μ j = 0,σ j = 10%,λ = 1,S 0 = 100.

(a) Generate a sample path for the stock price process S t on [0,3].

(b) Compute E[S t ], V ar(S t ) and the m.g.f. for S t .

(c) Compute E[(100 − S T ) + ],T = 3. (Using Monte Carlo simulation, and write down

the computer code)

(d) What is the probability for the stock price to exceed 105 at time 3? (Using Monte

Carlo simulation, and write down the computer code)

扫码加好友,拉您进群

扫码加好友,拉您进群 全部版块

全部版块 我的主页

我的主页

收藏

收藏