Markets are complete: For each state s, there is an Arrow-Debreu security that costs Ps at date 0 to purchase and pays one unit of the consumption good at date 1 if and only if state s occurs.

公司发行的任何证券(任何现金流)都可以在市场上找到替代品(可以被完全复制)。

No value to “financial marketing”:单纯通过分割现金流(e.g.创造出市场偏好的现金流)是不可能获得收益的。

1.3 假设Ⅲ

无套利,金融估值是理性的。

1.4 证明

Suppose that the firm’s assets will generate a random cash flow C next period (i.e., C(s) in state s). Today the firm issues securities Ki(s) against this cash flow (i=1,2,…,N is the index for different securities like equity, debt, etc.).

Denote Ci(s) as cash flow next period for security i(i=1,2,…,N) in state s, then the firm’s cash flow next period C(s)=∑i=1NCi(s) for each state s.

Complete Markets: For each future state of the world s, there exists an Arrow-Debreu security (i.e., one that pays $$ 1$ iff s occurs), trading at a market price of P(s).

By tracking portfolio using Arrow-Debreu security, the security i's value Ki=∑s=1SP(s)Ci(s).

Then the total value of this firm is V=i=1∑NKi=i=1∑Ns=1∑S[P(s)Ci(s)]=s=1∑Si=1∑N[P(s)Ci(s)]=s=1∑S[P(s)i=1∑NCi(s)]=s=1∑S[P(s)C(s)]

It means that the firm’s value is determined by it’s cash flow, independent of how it issues securities (M&M 1).

2. M&M and the cost of capital

【M&M Theorem Ⅱ】在M&MⅠ的假设下,WACC独立于资本结构。

证明:

PV=1+WACCE(CF)

由M&MⅠ,PV不随资本结构变化;由假设Ⅰ,CF不随资本结构变化。因此WACC与资本结构无关。

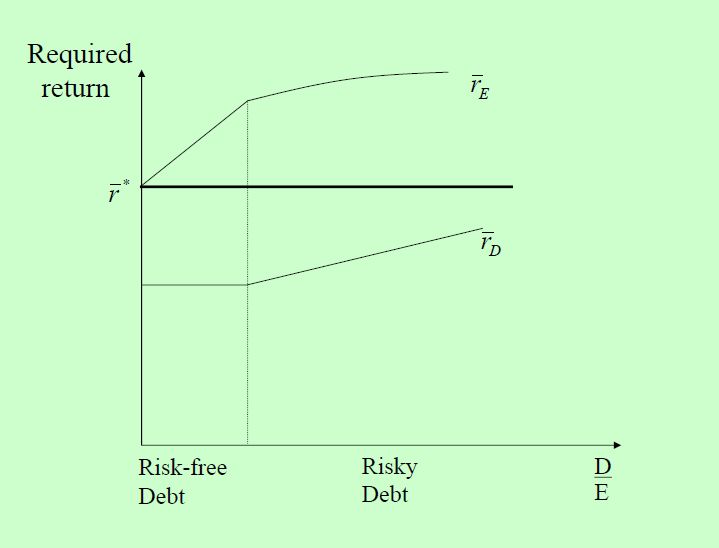

2.1 杠杆增加股权收益率

假设Ⅰ表明无税收,因此 WACC=rˉ∗=VDrˉD+VErˉE

从而股权收益率将随杠杆增大而增加(与上一章相符合) rˉE=rˉ∗+(rˉ∗−rˉD)ED

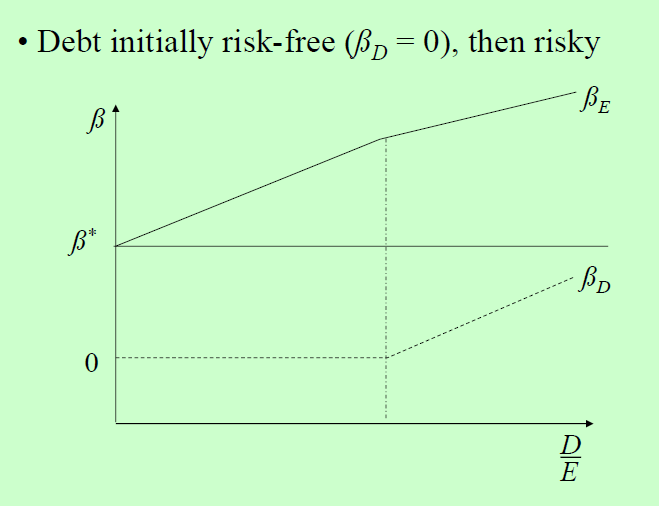

2.2 杠杆增加股权风险

The “asset beta” of firm β∗=VDβD+VEβE

Solve for βE βE=β∗+(β∗−βD)ED

从而杠杆将增加股权的系统性风险(即使债务无风险)。

扫码加好友,拉您进群

扫码加好友,拉您进群 全部版块

全部版块 我的主页

我的主页

收藏

收藏