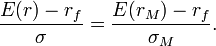

sigh 当年我也是不求甚解,所以不班门弄斧了,直接把'BEST ANSWER'搬给你,你就记着SML是用来看SINGLE ASSET,其上的资产TREYNOR RATIO 相同,都是相对于系统风险(BETA)来比的,就是下面的第一个公式,自己记忆里唯一用过的地方就是用来判断OVERVALUE, UNDERVALUE。 CML上都是MARKET PORTFOLIO 和 无风险资产的投资组合,其上的都是EFFIEICENT PTFL, SHARPE RATIO 相同

The capital market line (CML) is a line used in the capital asset pricing model to illustrate the rates of return for efficient portfolios depending on the risk-free rate of return and the level of risk (standard deviation) for a particular portfolio.

The CML is derived by drawing a tangent line from the intercept point on the efficient frontier to the point where the expected return equals the risk-free rate of return.

The CML is considered to be superior to the efficient frontier since it takes into

[size=100%][size=100%]account the inclusion of a risk-free asset in the portfolio. The capital asset pricing model (CAPM) demonstrates that the market portfolio is essentially the efficient frontier. This is achieved visually through the security market line (SML).

The security market line is a line that graphs the systematic, or market, risk versus return of the whole market at a certain time and shows all risky marketable securities.

The SML essentially graphs the results from the capital asset pricing model (CAPM) formula. The x-axis represents the risk (beta), and the y-axis represents the expected return. The market risk premium is determined from the slope of the SML.

The security market line is a useful tool in determining whether an asset being considered for a portfolio offers a reasonable expected return for risk. Individual securities are plotted on the SML graph. If the security's risk versus expected return is plotted above the SML, it is undervalued because the investor can expect a greater return for the inherent risk. A security plotted below the SML is overvalued because the investor would be accepting less return for the amount of risk assumed.

扫码加好友,拉您进群

扫码加好友,拉您进群 全部版块

全部版块 我的主页

我的主页

收藏

收藏